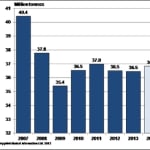

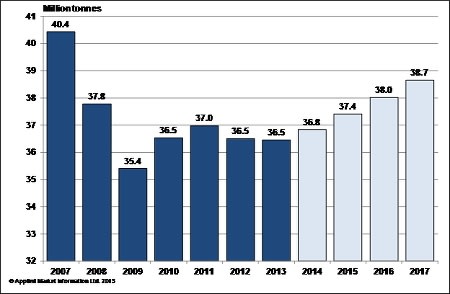

Polymer demand growth in Europe for 2013 is expected to be static compared with 2012, according to Applied Market Information Ltd., which has just published its 2013 European Plastics Industry Report. AMI calculates that the market for thermoplastics in Europe is currently 36.5 million tonnes, a volume that is still nearly 4 million tonnes less than the peak it hit in 2007. Although during 2010 and into 2011 the industry made a modest recovery from the devastating effects of the global downturn of 2008 and 2009, by the last quarter of 2011 the recovery was beginning to run out of steam in the face of the looming eurozone crisis. Although the drop in demand over 2012 and 2013 has been far less severe than in 2008-2009 - polymer producers and processors alike have been more savvy about managing their inventories and have not got caught out as they did in 2008 - the decline in government spending, manufacturing and consumer confidence still resulted in an overall contraction of polymer demand of just over 1% in 2012.

Polymer demand growth in Europe for 2013 is expected to be static compared with 2012, according to Applied Market Information Ltd., which has just published its 2013 European Plastics Industry Report. AMI calculates that the market for thermoplastics in Europe is currently 36.5 million tonnes, a volume that is still nearly 4 million tonnes less than the peak it hit in 2007. Although during 2010 and into 2011 the industry made a modest recovery from the devastating effects of the global downturn of 2008 and 2009, by the last quarter of 2011 the recovery was beginning to run out of steam in the face of the looming eurozone crisis. Although the drop in demand over 2012 and 2013 has been far less severe than in 2008-2009 - polymer producers and processors alike have been more savvy about managing their inventories and have not got caught out as they did in 2008 - the decline in government spending, manufacturing and consumer confidence still resulted in an overall contraction of polymer demand of just over 1% in 2012.However, whilst the market has undoubtedly been tough over the past five years, most companies have come through the downturn and continue to thrive and grow through the use of innovative technologies, material developments and new application gains. The discipline of the downturn has made companies cut costs, preserve cash and be judicious in their investments. Those that are suriving are increasingly thriving. Furthermore AMI views the industry now at the bottom of the cycle with demand expected to pick up again from 2014.

Germany, the engine of the European chemicals and plastic industry, has been the strongest of the West European markets. Although polymer consumption was down marginally in 2012 current market demand of around 8.2 million tonnes is only fractionally off the demand levels of 2007. The market has been sustained by the strength of its small and medium sized processors which have often developed leading roles in niche markets.